(Note: this table is illustrative and represents a simplification of industry trends)

Following the early wave of LBOs, the 1990s saw private equity firms focus on driving operational efficiencies in the businesses they acquired. In the 2000s, the corporate environment was generally much leaner, with more efficient balance sheets. Returns therefore had to come from somewhere else.

This saw a period of private equity firms focusing far more on how to create value for their portfolio companies by growing the top line through business expansion and product diversification. This is typically done in two ways: through strategic M&A and organic growth.

An M&A-led strategy, inorganic growth strategy, roll up strategy (also known as ‘buy-and-build’) can rapidly increase a business’s top line. A company can acquire revenues by buying up compatible businesses (or operations), sometimes competitors or adjacent firms, and merging them. Since larger platform companies tend to attract higher earnings multiples (a phenomenon referred to as ‘multiple arbitrage’ from the point at which the private equity fund invested to its realisation of the asset), this can increase returns for private equity funds.

Another important concept is multiple expansion, which occurs when a company’s valuation multiple increases over time. This can happen for two key reasons. First, the overall market may re-rate upward — a trend that benefitted the private equity industry during much of the 2010–2020 period, but which is far less prevalent today. Second, and more sustainably, the business itself becomes higher quality: it grows faster, operates more efficiently, or its financial performance becomes more predictable. For example, a company might improve its pricing model by moving from one-off license fees to recurring subscription revenue, or diversify geographically to reduce exposure to a single market. By making the companies we invest in not only bigger but demonstrably better, private equity firms can capture the benefits of this second, more durable form of multiple expansion.

But today, size alone no longer wins: a private equity firm is less likely to generate an attractive return simply by selling a business that is larger than the one it acquired. Companies must not only be bigger, but also better — with a sustainable future growth trajectory that is clear and compelling for the potential next owner. That’s why private equity’s focus has shifted in recent years decisively towards fundamental business improvement.

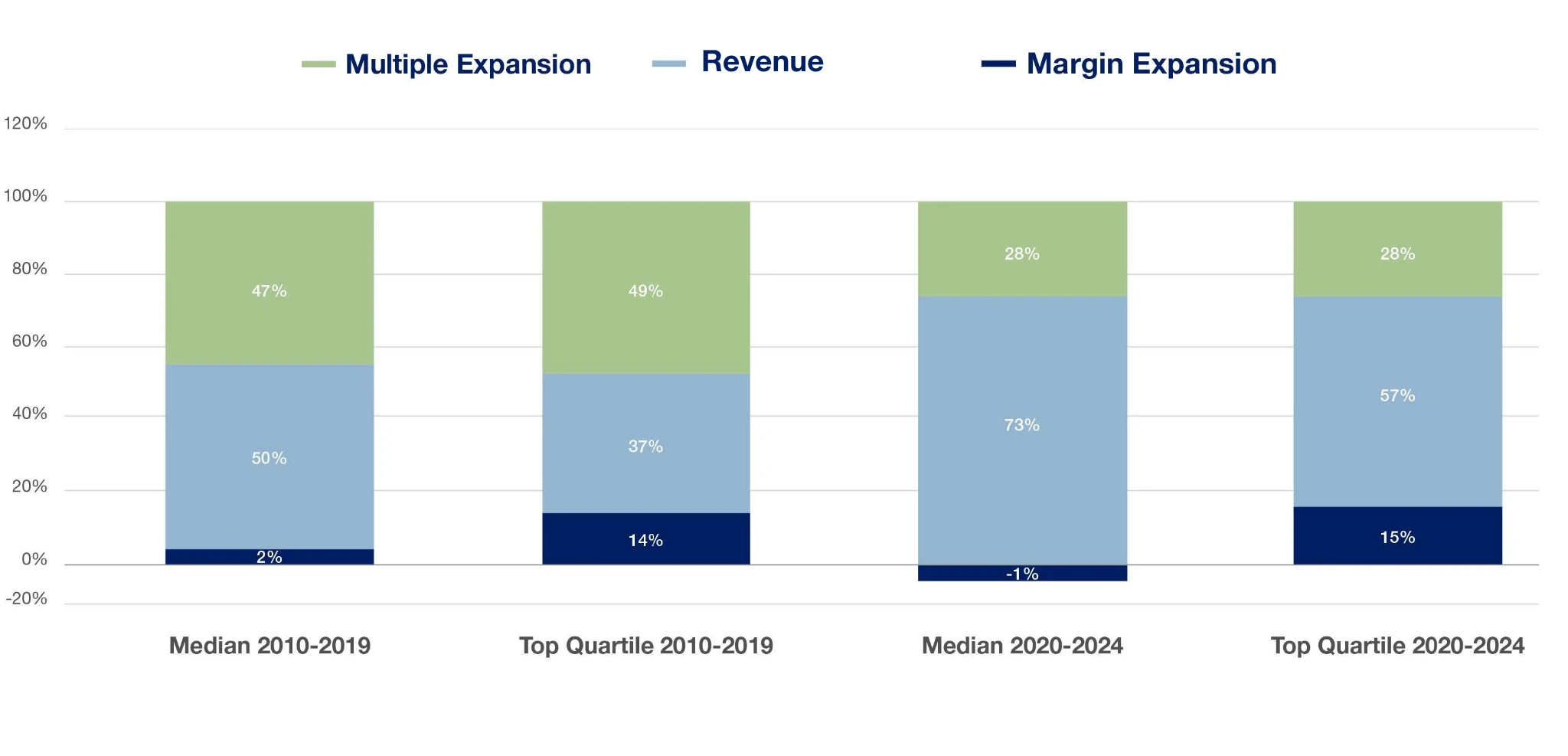

A 2024 study by strategy consultancy Simon-Kucher highlights the shift above. 46% of private equity returns now come from business improvement, eclipsing financial engineering and multiple arbitrages. Organic growth is the main engine — capturing new customers, deepening share of wallet, and investing in relentless innovation to stay ahead of the competition. As with many facets of private equity, averages mask a wide variety of approaches and outcomes. For instance, for Permira’s funds, 74% of returns have been driven by top-line growth and EBITDA margin growth in our portfolio companies.

Traditional value creation strategies still count — multiple arbitrage and margin expansion through operational efficiency remain a focus for buyout firms. But in an investment environment that is becoming increasingly complex, those firms that can blend operational discipline with a deep understanding of growth drivers will be able to successfully accelerate growth through cycles.

Fig 2: Operational improvement continues to grow as the primary driver of private equity value creation